【CFA三级笔记】资产配置:第一章 资本市场预期(宏观分析)

目录

1 Challenges in Capital Market Forecasting★★

2 Economic and Market Analysis

2.1 Exogenous Shocks to Growth 外部冲击对经济增长的影响(经济增长中不可预测的部分)★

2.2 Growth Analysis to Capital Market Expectations 资本市场预期对经济增长影响的分析(经济增长中可以预测的部分)

2.2.1 经济增长趋势分析在形成资本市场预期中的应用★★★

2.2.2 经济预测的主要方法★★★

2.3 经济周期分析

2.3.1 经济周期的五个阶段分析★★★

2.3.2 通货膨胀对资产收益率的影响★★

2.4 货币政策和财政政策分析

2.4.1 财政政策

2.4.2 货币政策★★★

2.4.3 货币政策与财政政策的联动影响★★★

2.5 International Interactions 国际互动

2.5.1 Macro Linkages宏观经济联系

2.5.2 Interest Rate/Exchange Rate Linkages 利率/汇率联系★

1 Challenges in Capital Market Forecasting★★

这一块可能考主观题,因为以前考过。

考法:①给你一段描述,问你反应了什么challenge;②某一个问题可能带来什么样的后果

| 1. Limitations to using economic data 经济数据的局限性 | ① Time lag: older data increase the uncertainty concerning the current economy 经济数据有滞后性 ② Revision 统计数据会更新和修订 ③ Change in definition or calculation method 经济数据的定义和计算方法会改变 ④ Re-base 一些经济金融数据供应商会调整基准年份 |

| 2. Data measurement errors and biases 数据测量错误和偏差 | ① Transcription errors 转录错误(数据收集和记录出错) ② Survivorship bias 幸存者偏差(主观题★★★),Data reflects only entities that survived to the end of the period → 高估收益。典型:alternative investment (e.g. hedge fund) ③ Appraisal data 评估数据/平滑数据(主观题★★★)。For assets without liquid public markets,appraisal data are used in leu of transaction data → Volatility被低估,Correlations with other assets被低估。典型:real estate |

| 3. Limitation of historical estimates 历史估计的局限性(★★★)(主观题) | ① Historical data may not be representative of the future period 历史不代表未来 ② The non-stationarity of Historical Data 历史数据的非平稳性(当你说一列数据是非平稳的(non-stationary)时,意味着这列数据的统计特性,如均值、方差、自相关性等,会随时间推移而发生变化。换句话说,它的分布规律不是固定的,而是依赖于时间)——Changes in Regime:different parts of a data reflect different underlying statistical properties

③ Whether the data are normally distributed (Historical asset returns routinely exhibite skewness and fat tails 历史数据表现出来的往往是有偏的,肥尾的,但是我们的模型通常假设正态分布)

|

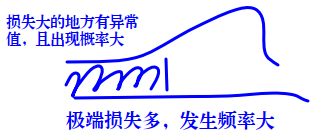

| 4. Ex Post risk as a biased measure of Ex Ante risk (peso problem) 事后风险是事前风险的有偏估计(比索问题)(★★)(主观题) | ① Whether asset prices reflected the possibility of a very negative event that did not materialize during the period. ("peso problem."): 事后分析历史经济数据时,分析师会忽略那些小概率的极端负面事件(negative events)对市场的影响,造成事前风险被低估、事前收益被高估。 -- high ex post returns that reflect fears of adverse events that did not materialize. -- underestimate ex ante risk and overestimate ex ante anticipated returns.

② lf our data series includes even one observation of a rare event → overstate the likelihood of such events happening in the future. 若选取的数据时间段正好包含极端事件的观察值,则可能会高估极端负面事件在未来的发生概率,进而造成风险被高估、收益被低估。 |

| 5. Biases in analyst's methods 分析方法的偏差(★) | ① Data Mining Bias数据挖掘偏差:将巧合视作规律

② Time Period Bias 时间段偏差:指研究分析的模型或结论只适用于特定时间段 |

| 6. Ignore conditioning information 忽略条件信息 | 资产的风险与收益特征会随着经济周期的改变而发生变化。基于历史数据统计得到的风险和收益指标可能包含多个经济周期条件。因此,在预测相关指标时,应对不同经济条件下的资产表现进行分类讨论,不能一概而论。

Unconditional forecasts, which dilute this information by averaging over environments, can lead to misperception of prospective risk and return. “无条件预测” 是一种不区分当前 / 未来经济 / 市场环境、直接对历史数据进行 “整体平均” 的预测方法。无条件预测将 “不同环境下差异极大的风险收益数据” 混在一起平均,导致原本与环境强关联的 “关键特征信息” 被 “拉平”,最终丢失了 “环境→资产特征” 的对应关系。 |

| 7. Misinterpretation of Correlations 相关系数的错误解读 (★) | ① 变量关系的错误解读:相关关系并不代表因果关系

② 相关系数的错误解读 |

| 8. Psychological Traps 心理偏差(★) | ① 锚定偏差(Anchoring Bias):决策时过度依赖最初接触的信息(锚点),后续判断难以脱离该锚点的影响(被 “第一个看到的信息” 绑住了,比如 “这只股票之前涨到过 100 元,现在 60 元肯定便宜”),而非基于全面信息调整 → 解决办法:consciously avoid premature conclusion,更全面的搜集信息 ② 现状偏差(Status Quo Bias):倾向于维持当前的状态或选择,即使存在更优的替代方案,也因抵触改变而不愿调整,do nothing → 解决办法:discipline effort ③ 确认偏差(Confirmation Bias):主动寻找、关注能印证自身已有观点的信息,刻意忽略或否定与自身观点相悖的证据(先有了 “我是对的” 的想法,再找证据证明,比如 “我觉得新能源能涨,所以只看新能源的利好新闻”) → 解决办法:exam all evidence & debate with others ④ 过度自信偏差(Overconfidence Bias)(略) ⑤ 谨慎偏差(Prudence Bias)→ 解决办法:identify plausible scenarios ⑥ 易得性偏差(Availability Bias)→ 解决办法:base conclusions on objective evidence and analytical procedures. |

| 9. Model and input uncertainty | 在进行分析时,通常会遇到三种类型的不确定性:模型不确定性、参数不确定性和输人不确定性 ① 模型的不确定性(model uncertainty)是指分析所选模型可能存在结构或概念性的错误 ② 参数不确定性(parametric uncertainty)是指由于量化模型的参数估计总是存在一定的错误,因此模型预测结果可能存在错误 ③ 输入不确定性(input uncertainty)是指由于模型的输入值可能错误,继而造成预测结果错误 |

2 Economic and Market Analysis

Economic output has both cyclical and trend growth components:(1) Trends are about long-term averages;(2) cycles are about shorter-term movements and turning points.

2.1 Exogenous Shocks to Growth 外部冲击对经济增长的影响(经济增长中不可预测的部分)★

给你一个Shock,问你这个是促进经济增长还是迟滞经济增长?

| Policy Changes 政策变化 | Pro-growth government policies include: Sound fiscal policy(转移支付transfer payment属于促进经济增长的政策), minimal intrusion on the private sector, encouraging competition within the private sector, support for infrastructure and human capital development, sound tax policies, and removing trade barriers. |

| New products and technologies 新产品和新技术 | enhances potential growth |

| Geopolitics 地缘政治 | 一国政治环境的稳定会降低投资风险,继而吸引外资,促进当地经济发展。而地缘政治冲突(geopolitical conflict)的发生会导致资源转移,降低经济生产效率,从而减缓经济增长。例如,由于A、B两国发生军事冲突,两国加大军费开支,进而对两国的经济均造成影响。 |

| Natural disasters 自然灾害 | 默认自然灾害会破坏生产能力。从短期来看,自然灾害可能会降低增长,但如果在重建过程中,使用更高效的设施取代旧产能,它实际上可能会促进长期增长。 |

| Natural resources/critical inputs 自然资源或生产要素的发现 | 自然资源或关键生产要素的发现会提高生产要素水平,降低生产要素的成本,促进当地经济发展。例如,大型油田的发现会提高石油供给量,降低石油价格,继而降低企业的生产成本,促进经济增长。 |

| Financial crises 金融危机 | Financial crises arise when market participants lose confidence in others' ability(or willingness) to meet their obligations and cease to provide funding. A financial crisis may affect the level of output and the trend growth rate. |