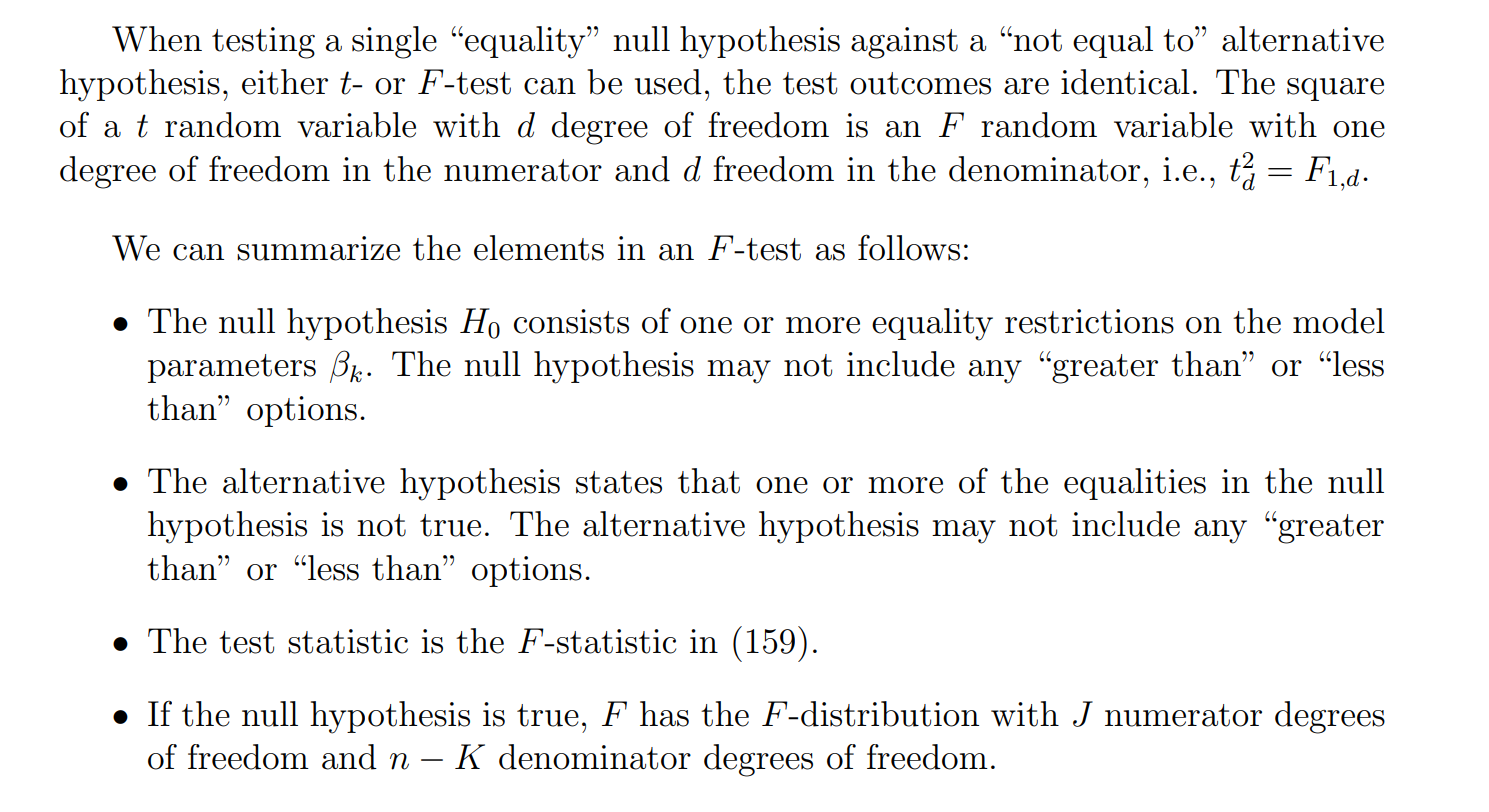

Further inference in the multiple linear regression model

Joint hypothesis testing

-

Simple null hypothesis → involves a restriction on one sign (<,=,>) only (e.g.H0:β2=0).(e.g. H_0: \beta_2 = 0).(e.g.H0:β2=0).

-

Joint null hypothesis → involves two or more restrictions at the same time (e.g.H0:β2=0, β3=0, β4=0).(e.g.H_0: \beta_2 = 0, \; \beta_3 = 0, \; \beta_4 = 0).(e.g.H0:β2=0,β3=0,β4=0).

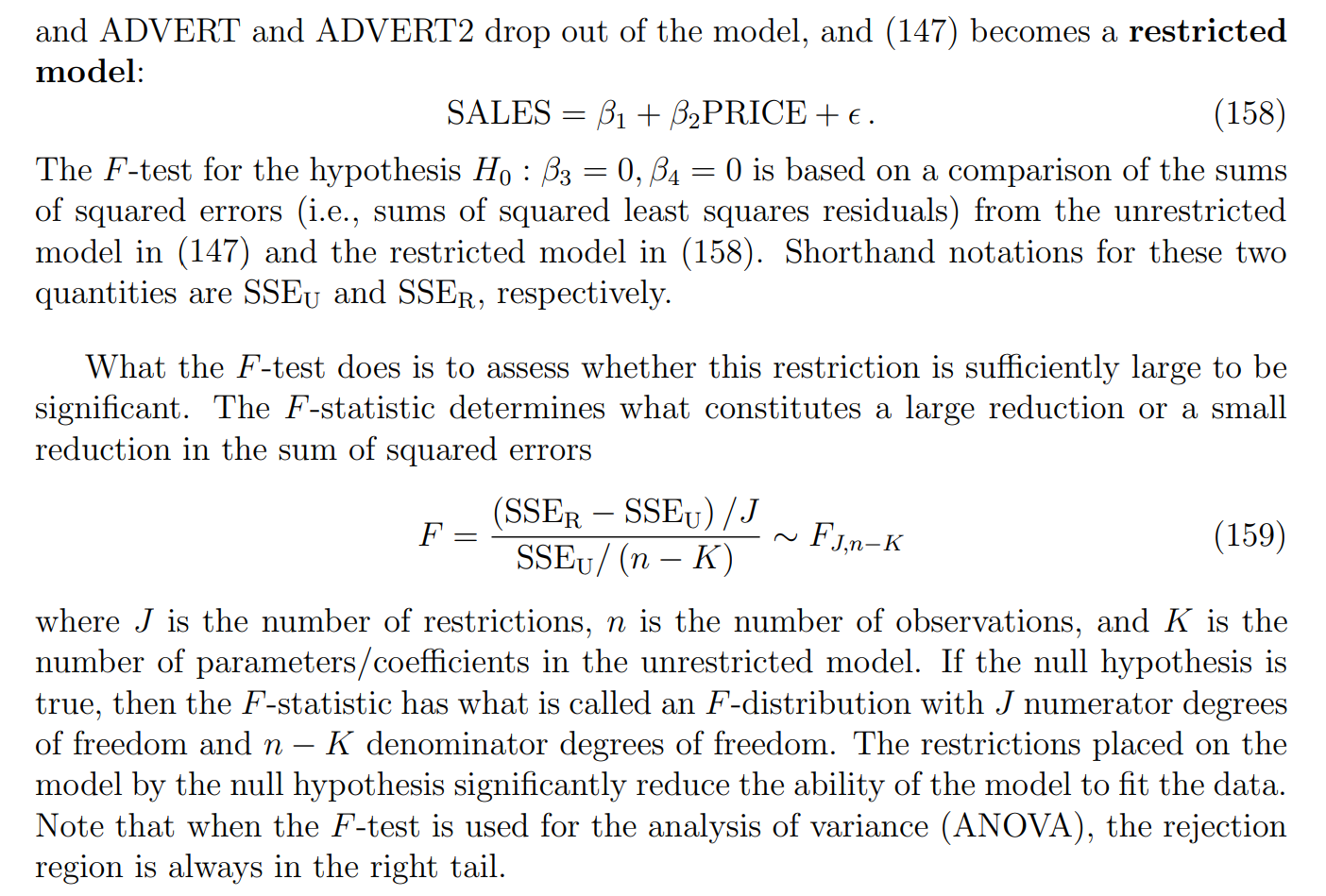

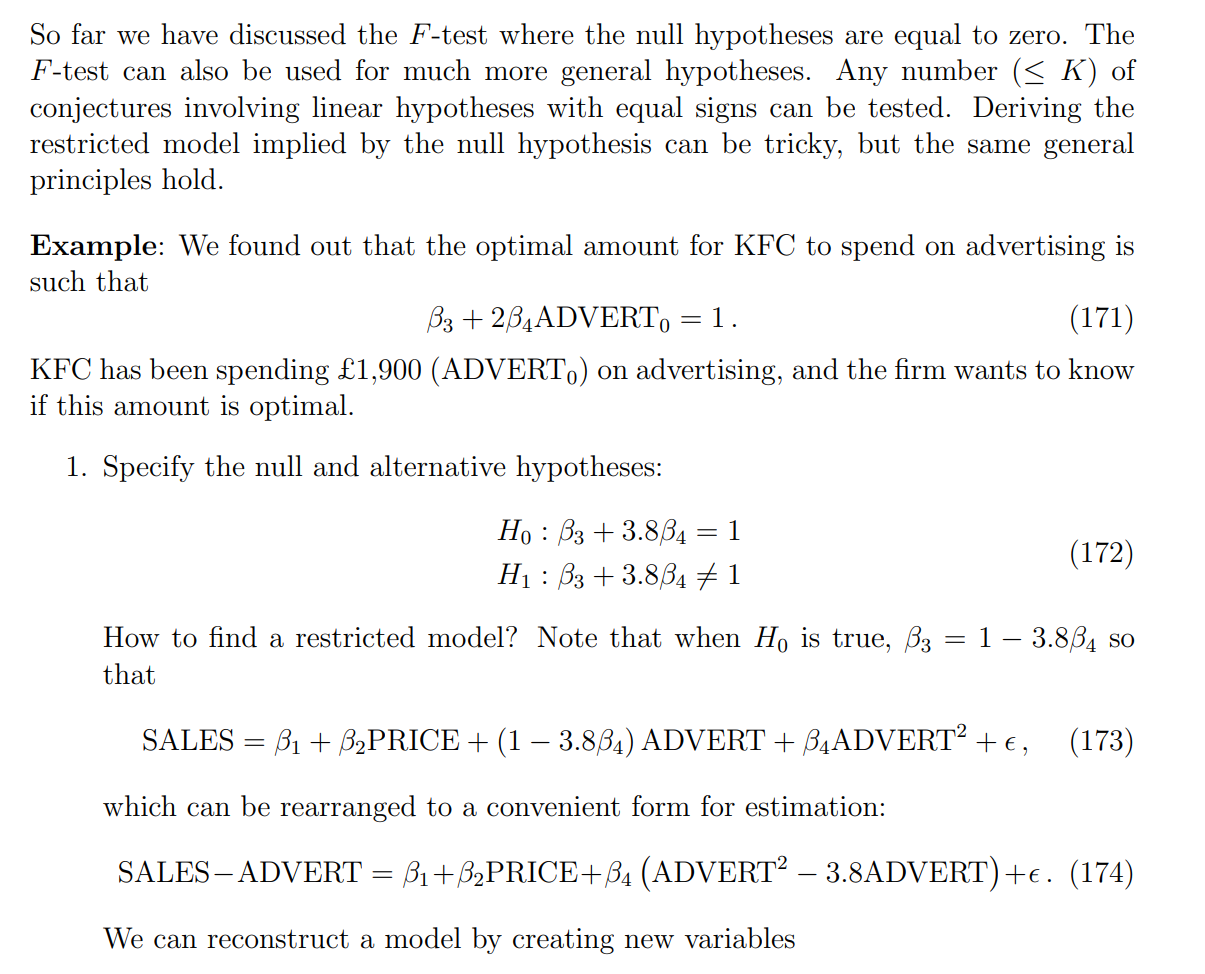

Testing the effect of advertising: The F-test

restricted model : βi=0\beta_{i}=0βi=0

-

An unrestricted model is the “full” regression specification, where you estimate all parameters freely without imposing any restrictions. For example, if your regression is

y=β0+β1x1+β2x2+β3x3+uy = \beta_0 + \beta_1 x_1 + \beta_2 x_2 + \beta_3 x_3 + uy=β0+β1x1+β2x2+β3x3+uthen the unrestricted model estimates β0,β1,β2,β3β0,β1,β2,β3β0,β1,β2,β3 all at once.

-

A restricted model is the version of the model after you impose the null hypothesis restrictions. For instance, if

H0:β2=β3=0H_0: \beta_2 = \beta_3 = 0H0:β2=β3=0then the restricted model reduces to

y=β0+β1x1+uy = \beta_0 + \beta_1 x_1 + uy=β0+β1x1+ubecause the restrictions eliminate x2x_2x2 and x3x_3x3 from the regression.

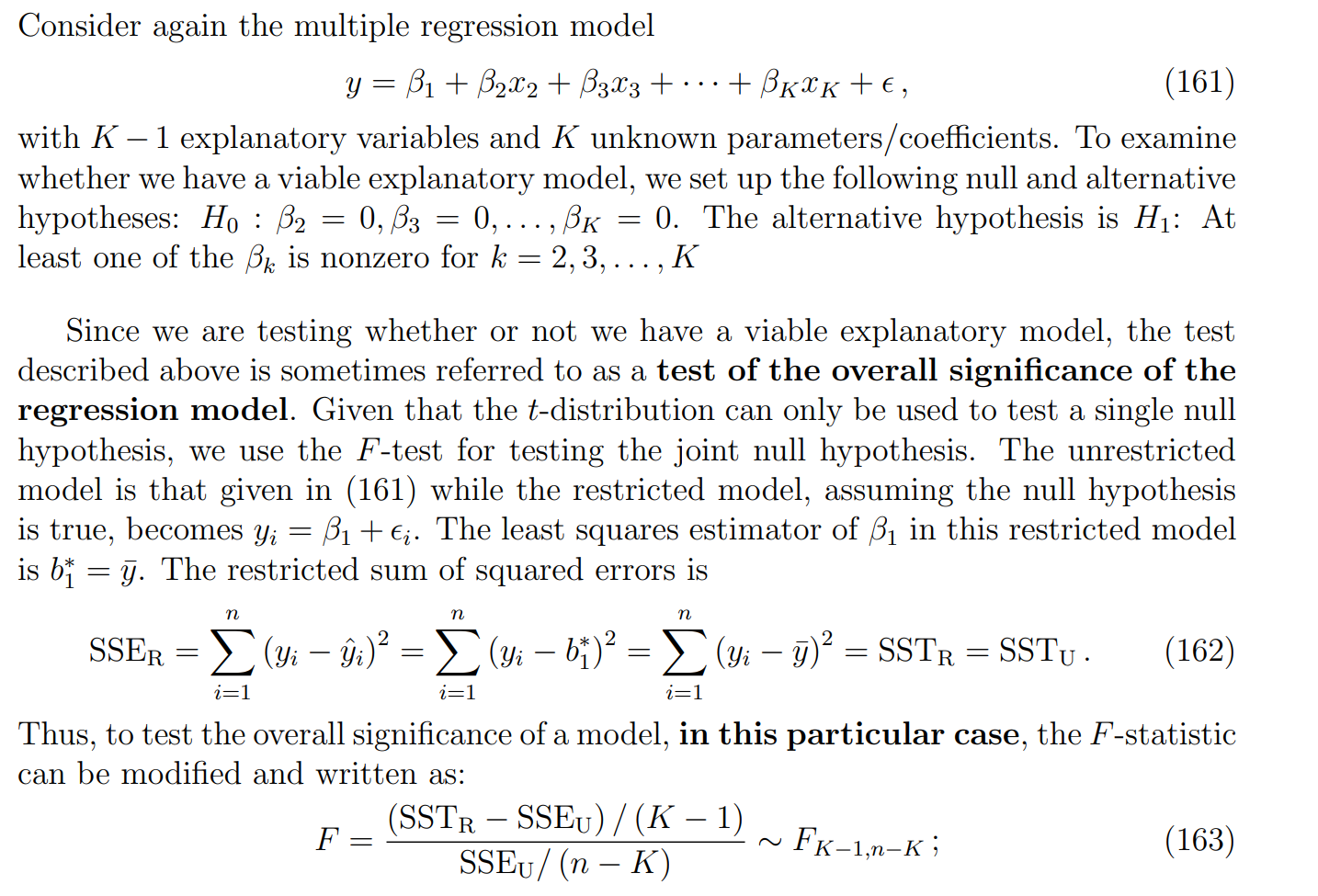

Testing the overall significance of the model

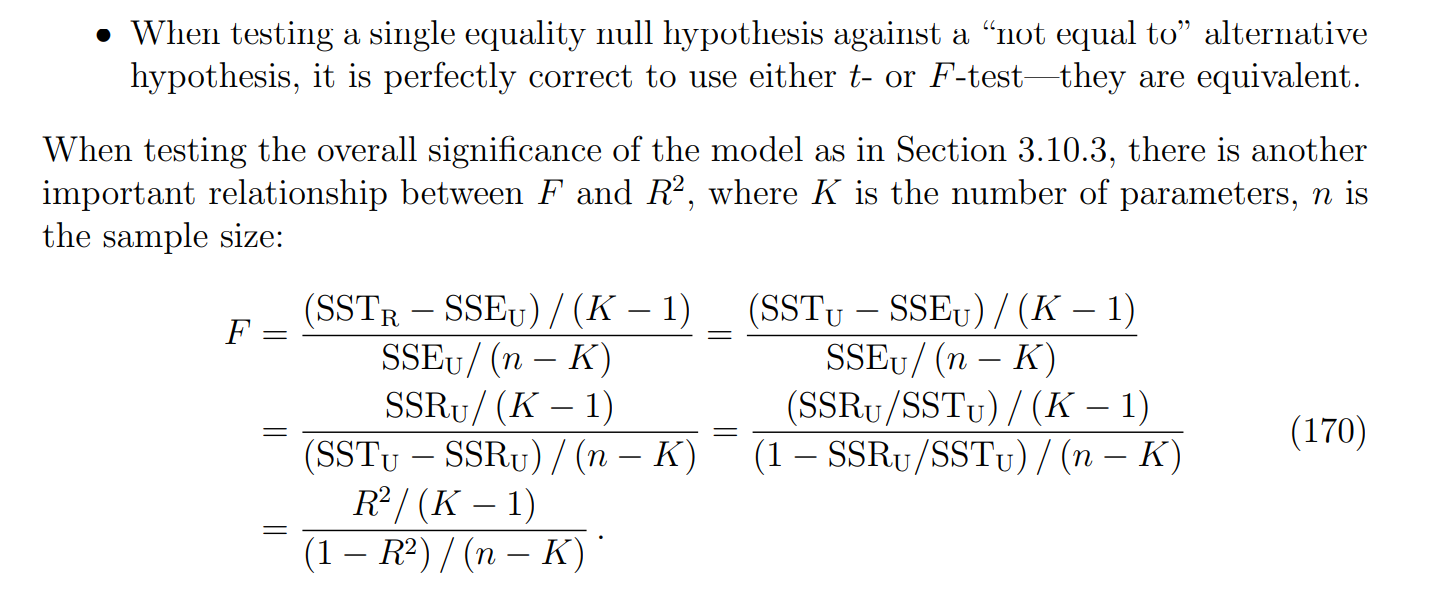

t-test and F-test

More general F-tests

-

The F-test is the standard way to test any set of linear restrictions, not just “all equal to zero.”

-

Here the restriction links two parameters (β3\beta_3β3 and β4)β_{4})β4) together. That means you cannot just look at a single t-statistic — the test requires accounting for covariance between estimators.

-

The F-test compares restricted model vs. unrestricted model fit:

-

Unrestricted model: estimate β3,β4\beta_3, \beta_4β3,β4 freely.

-

Restricted model: force β3=1−3.8β_{3}=1−3.8β3=1−3.8

-

What “restricted model” really means

-

The restricted model is any regression model you get after imposing the null hypothesis.

-

If the null says βj=0\beta_j = 0βj=0, then yes: the restricted model is simply dropping that variable.

-

But in general, the null may say something else, e.g.

β3+3.8β4=1\beta_3 + 3.8\beta_4 = 1β3+3.8β4=1

That is not a zero restriction, but it’s still a restriction on parameters.

So: restricted model ≠ only β=0. Instead, it means “the model under the null hypothesis.”

Why substitution is needed

When the null hypothesis involves a linear combination (like β3+3.8β4=1:\beta_3 + 3.8\beta_4 = 1:β3+3.8β4=1:

-

You cannot just delete regressors, because neither β3\beta_3β3nor β4\beta_4β4 is zero.

-

Instead, the restriction ties them together, so one becomes dependent on the other.

-

To build the restricted model, you must substitute that relationship back into the regression equation.

That’s why in your KFC example, they replaced β3\beta_3β3 with 1−3.8β41−3.8β_{4}1−3.8β4.

Substitution is exactly the way to re-express the restricted model so it still looks like a valid regression: